Private Mortgage Insurance changes by the Federal Housing Administration

Print

Print Email

EmailChanges made to PMI on a residential mortgage.

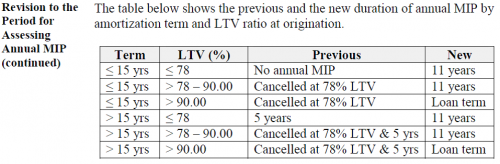

The Federal Housing Administration (FHA) recently made changes to the length of time that Mortgage Insurance is retained on a home loan. Mortgage Insurance, also known as Private Mortgage Insurance or PMI, is the premium paid by the borrower that protects the lender from losing the money loaned in case the borrower defaults on the loan. Typically, Mortgage Insurance is added to an FHA loan when a borrower puts less than 20 percent of a down payment towards the purchase of a home. Mortgage Letter 2013-04, published by the U.S. Department of Housing and Urban Development, outlines the changes in the Mortgage Insurance premiums that took place June 3, 2013. The following chart outlines the changes that have been made:

Borrowers who are obtaining a home loan from FHA will have to pay an upfront premium and an ongoing monthly premium, in some cases for the life of the loan. In the past, when a borrower put down less than 20 percent towards the purchase of the home, the PMI would cease to be paid after the borrower reached a maturation of 5 years with a loan-to-value of 78 percent. However, this has since changed. Borrowers who put down less than 10 percent towards the purchase of a home will pay the Mortgage Insurance for the life of the loan. This is a big change as borrowers can no longer count on that premium dropping off after 5 years, which in turn would cause the monthly house payment to decrease. Borrowers who put down less than 10 percent must budget to retain the mortgage insurance for the life of the loan.

In the past, borrowers who put down upwards of 20 percent had no Mortgage Insurance Premium to contend with. The new guidelines state that PMI would be placed on the loan and paid for 11 years.

Michigan State University Extension offers homebuyer education seminars that educate potential homebuyers on the home buying process. Borrowers must educate themselves to be aware of all the changes in this new housing finance culture. The most educated consumer can become the most fiscally responsible consumer.