Fertilizer price trends in the second half of 2017

Print

Print Email

EmailThe retail prices of all major fertilizers remained relatively low and stable in the second half of 2017, according to USDA statistics.

The approximate retail prices for bulk purchases of major fertilizers per ton, published in the Dec. 7, 2017, USDA Illinois Department of Agriculture Market News Report are shown in Table 1.

|

Table 1. Prices for major fertilizers |

|

|---|---|

|

Fertilizer source |

Price |

|

Diammonium phosphate (DAP) |

437 |

|

Monoammonium phosphate (MAP) |

444 |

|

Potash |

326 |

|

Urea |

341 |

|

Urea-Ammonium Nitrate (UAN 28%) |

221 |

|

Anhydrous ammonia |

418 |

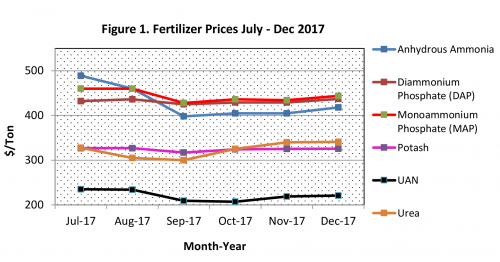

The prices of all fertilizers are 5-15 percent lower than the corresponding 2016 prices. The monthly price trends for the second half of 2017 are shown in Figure 1. The prices remained relatively stable. Anhydrous ammonia showed the steepest decline from July to September. The fertilizer industry is historically cyclical and currently going through a down cycle. The low fertilizer prices have helped farmers reduce production costs compared to other inputs. Despite the current fertilizer market stability, unforeseen changes in global demand or supply may cause price fluctuations.

Figure 1. Fertilizer prices for the second half of 2017 ($/ton). Data source: USDA-Illinois Dept. of Ag Market News Springfield, Illinois, cash prices for bulk purchases, granular form unless noted.

Michigan State University Extension recommends being aware of price fluctuations over time and taking advantage of purchasing options. Some proactive farmers prefer to pre-order and lock in phosphorus and potassium fertilizer for the following season when off-season prices are favorable. The low phosphorus and potassium fertilizer prices should also be an incentive for growers to apply phosphorus and potassium at buildup rates on fields that are currently below the critical soil test levels, following the MSU fertilizer recommendations.